If you have been looking for a way to earn passive income from solar energy in the Philippines — without building a single solar panel — then CREIT stock is probably on your watchlist.

And it should be. Citicore Energy REIT Corp. is the country’s first and largest renewable energy REIT stock listed on the Philippine Stock Exchange. It leases land and operational solar plants to energy companies under long-term contracts, then passes most of that rental income directly to shareholders as dividends. That is the promise of this stock — and for many investors, it sounds almost too good to be true.

This CREIT stock Philippines analysis will walk you through what the company does, how its financials look for 2026, how we arrived at our own independent valuation, and — most critically — what you need to know before deciding whether the current price is actually a safe place to enter.

Here is the honest version. No hype. Just the numbers and what they mean.

But first, a word about the most common mistake beginner investors make with REITs: they look at the dividend yield, see a number they like, and buy without checking whether that yield is actually safe or whether the price already reflects too much optimism. That is the gap this article helps you close.

How do you really invest in Philippine stocks the right way?

Many Filipinos dream of investing—but don’t know where to start, which stocks are safe, or when the right time is. The Truly Rich Club by Bo Sanchez is designed for exactly that situation. Every month, you’ll receive specific stock picks, updated buy-below prices, and simple guidance that doesn’t require a finance degree. Thousands of Filipinos have already started investing with confidence—you could be next.

What Is a REIT — And What Makes CREIT Different?

Before we dig into the numbers, let us make sure you understand what kind of company we are dealing with.

A REIT — Real Estate Investment Trust — is a company that owns income-generating properties and is legally required by Philippine law to distribute at least 90% of its distributable income to shareholders as dividends. Think of it like this: instead of buying land and renting it out yourself, you buy shares in a REIT and receive your portion of the rental income it collects from a large portfolio of properties.

Most REITs in the Philippines own office towers, shopping malls, or commercial buildings. CREIT is different. It is not a traditional commercial property REIT. Instead, it earns income by leasing land to solar farm developers and operators, as well as leasing out fully operational solar plants to independent energy companies. Its revenue is anchored on guaranteed base rental income under long-term lease contracts — not market prices, not electricity spot prices, and not mall occupancy rates.

CREIT is majority-owned and sponsored by Citicore Renewable Energy Corporation (CREC), one of the Philippines’ largest renewable energy developers. That sponsorship matters because it provides both a credibility anchor and a potential future pipeline of assets that could be injected into CREIT over time.

Its current portfolio consists of one operational solar power plant and thirteen land parcels, spread across multiple provinces, covering over 7.1 million square meters of gross leasable area. Total installed capacity currently sits at 145 megawatts.

3 Key Developments Every CREIT Investor Should Know in 2026

1. Revenues and Income Held Steady — But Growth Is Flat

CREIT’s full-year 2025 revenues came in at approximately ₱1.88 billion, essentially unchanged from the prior year. Net income also held flat at around ₱1.43 billion. This was not a surprise — management had already guided for minimal top-line growth, and the slight revenue dip was driven by a non-cash accounting adjustment related to the extension of lease terms on its Lumbangan landholdings, not by any deterioration in actual cash collections.

The key takeaway: CREIT’s business is predictable and stable. But predictable also means slow-growing. Revenue growth for the next three years is projected at approximately 1% per year. If you are hoping for rapid dividend increases from organic growth alone, this stock will likely disappoint.

2. A 1GW Solar Asset Infusion Is Being Planned — But Timeline Is Unclear

This is the most significant development on CREIT’s radar for 2026. Management has announced plans to infuse 1 gigawatt of solar plant assets from its parent company into the REIT. To put that in perspective, CREIT’s current installed capacity is 145MW — so a 1GW infusion would represent a portfolio nearly eight times larger than what it has today.

That kind of growth would be transformational. If successfully executed, it would dramatically increase CREIT’s distributable income and dividend-paying capacity.

But here is the catch: as of the latest update, management has confirmed that there is no fixed timeline, no confirmed deal size, and no finalized terms. The infusion is being monitored and planned, not executed. Management has signaled that instead of taking on new debt to fund the acquisition, they may pursue a property-for-share swap — which means new shares would be issued to the parent company in exchange for the solar assets. That approach would avoid additional borrowing but could dilute existing shareholders.

The AEI — or Asset Enhancement and Injection — pipeline from the sponsor is real and large. But real does not mean imminent. For income investors who need certainty in the near term, this is a meaningful risk factor.

Note: AEI (Asset Enhancement and Injection) refers to the process where a REIT’s parent or sponsor transfers additional income-generating properties into the REIT — growing the portfolio and potentially increasing dividends for existing shareholders.

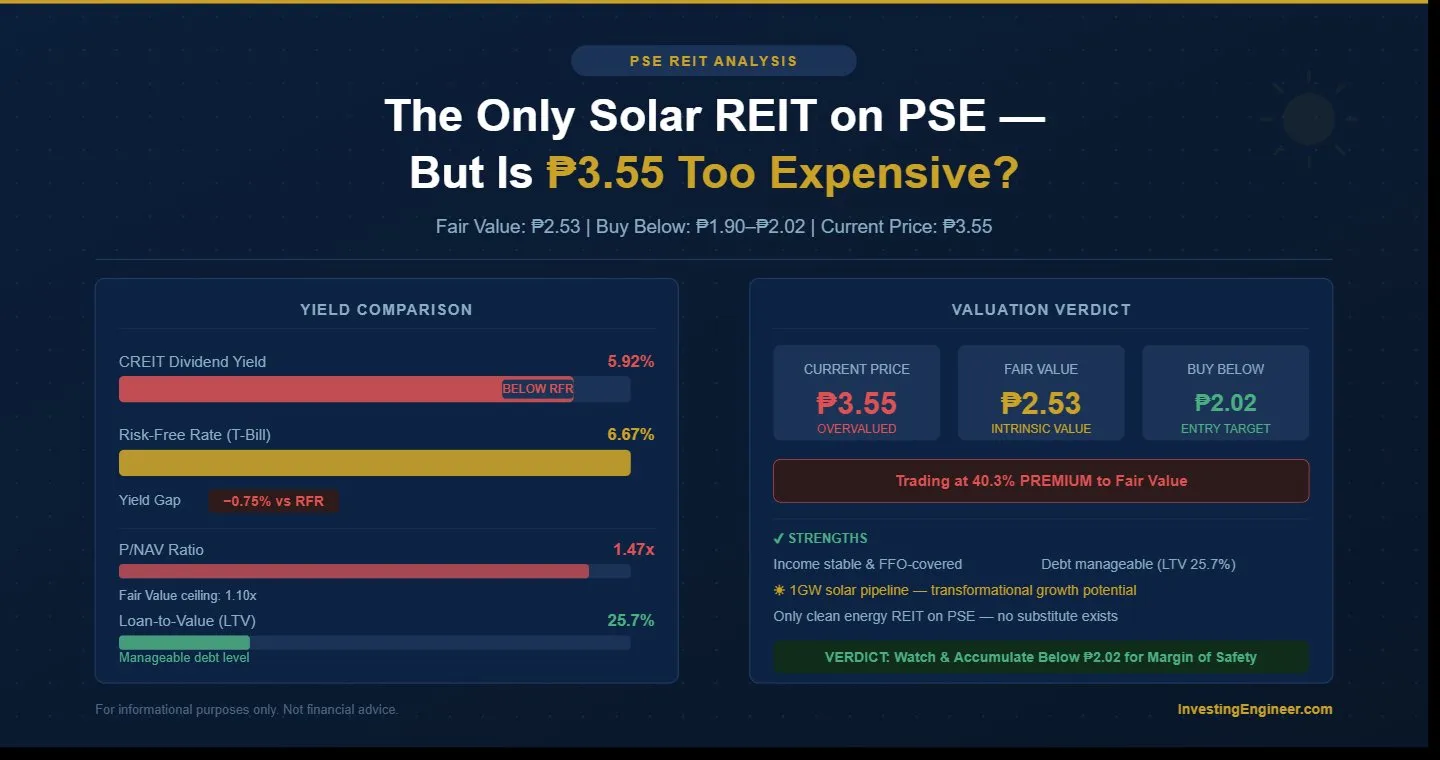

3. The 2026 Dividend Yield Is 5.92% — Below the Risk-Free Rate

CREIT is projected to distribute approximately ₱0.21 per share in dividends for 2026 — a modest 4.1% increase from the ₱0.20 distributed in 2025. At the current share price of ₱3.55, that translates to a forward dividend yield of approximately 5.92%.

That is where things get uncomfortable. The Philippine 10-year government bond yield is currently around 6.67%. That means a risk-free government bond pays you more than CREIT does at today’s price — without any company-specific risk. That is not a good sign for income investors, and it is the first warning flag we flag in our valuation below.

Is CREIT Stock Worth Buying at ₱3.55? Our Independent Valuation

CREIT is a REIT, which means we do not value it the same way we would a regular company. We do not use standard earnings per share. Instead, we use a three-step framework built around income-generating power, asset value, and a multi-dimensional margin of safety check.

Understanding FFO — The Right Measuring Stick for REITs

For most stocks, we look at earnings per share — how much profit the company makes for each share you own. For REITs, the more meaningful number is FFO, or Funds From Operations.

Here is why this matters: REITs own physical properties that depreciate on paper every year. That depreciation reduces reported net income — but the buildings and land are not actually losing real-world value. FFO adds that depreciation back to net income, giving you a cleaner picture of how much actual cash the REIT is generating. Think of FFO as the REIT version of EPS — the number that tells you what the business truly earns in cash.

For CREIT, we estimate 2026 FFO per share at approximately ₱0.241, by taking projected net income per share and adding back depreciation and amortization.

Step 1 — Dividend Yield Anchor: The First Safety Check

The simplest and most intuitive way to assess whether a REIT is fairly priced is to compare its dividend yield against the Philippine 10-year government bond rate. This tells you whether the REIT is actually paying you more than a risk-free alternative — and by how much.

A yield spread of at least 2%–3% above the T-bond rate is considered a healthy margin of safety. It means you are being adequately compensated for the added risk of owning a stock rather than a government bond.

| Metric | Value |

| CREIT Forward DPS (2026E) | ₱0.21 per share |

| Current Share Price | ₱3.55 |

| Forward Dividend Yield | 5.92% |

| PH 10-Year T-Bond Yield | ~6.67% |

| Yield Spread | −0.75% (NEGATIVE) |

| Target Minimum Spread | +2.00% to +3.00% |

| Verdict | ❌ INADEQUATE — Risk-free bond pays more |

At the current price of ₱3.55, CREIT’s dividend yield is not only below the ideal target — it is actually lower than what you could earn from a government bond. This alone is a meaningful caution flag for income-focused investors.

Step 2 — Price-to-FFO Valuation

For a well-run Philippine REIT, the appropriate multiple ranges from 12x to 16x FFO. Here is how we adjusted that multiple specifically for CREIT:

| Factor | Adjustment | Rationale |

| Base P/FFO Range | 12x – 16x | Philippine REIT baseline |

| Strong sponsor (CREC) with large AEI pipeline | +1x | Credible sponsor |

| Long-term land leases, high income predictability | +1x | Low income volatility |

| Rising interest rate environment (PH T-bond ~6.67%) | −2x | REITs less attractive at higher rates |

| No confirmed timeline or terms on 1GW asset infusion | −1x | Growth catalyst is uncertain |

| Adjusted P/FFO Multiple | 11x | Conservative |

| FFO-Based Fair Value (₱0.241 × 11x) | ₱2.65 per share | |

Step 3 — NAV Cross-Check

As a second reference point, we compare the current share price to CREIT’s Net Asset Value — essentially what the company’s properties and assets are worth after subtracting its obligations. This gives us a sense of whether we are paying more or less than the underlying asset value of the portfolio.

Based on publicly available data, CREIT’s implied NAV per share is approximately ₱2.41. At the current price of ₱3.55, the stock is trading at roughly 1.47x NAV.

| Metric | Value |

| Implied NAV per Share | ~₱2.41 |

| Current Price | ₱3.55 |

| P/NAV Ratio | ~1.47x |

| Fair Value Range | 0.85x – 1.10x NAV |

| NAV-Based Fair Value | ₱2.41 per share |

| Verdict | ❌ Trading at 47% premium to NAV |

A P/NAV above 1.10x typically requires strong justification — either very high income growth or a confirmed, imminent asset injection. For CREIT, the 1GW infusion is real but unscheduled, and income growth is projected at around 4% annually. A 47% premium to NAV is difficult to justify on those fundamentals alone.

Step 4 — Blended Fair Value and Buy Below Price

| Component | Weight | Value |

| FFO-Based Fair Value | 50% | ₱2.65 |

| NAV-Based Fair Value | 50% | ₱2.41 |

| Blended Fair Value | — | ₱2.53 |

| Buy Below Price (20% MOS) | −20% | ₱2.02 |

| Buy Below Price (25% MOS) | −25% | ₱1.90 |

| Current Price | — | ₱3.55 — ABOVE FAIR VALUE |

Note: MOS stands for Margin of Safety — the buffer we apply below fair value to protect against errors in our estimates and unexpected events. The wider the margin, the more protection you have.

Margin of Safety Assessment — 5 Dimensions

For REITs, margin of safety is not just a single number. It comes from five dimensions that tell you whether your investment is truly protected across multiple risk angles. Here is how CREIT scores right now:

| Safety Check | What We Measure | CREIT Reading | Threshold | Verdict |

| 1. Yield Spread | REIT dividend yield vs 10-yr T-bond | 5.92% − 6.67% = −0.75% spread | ≥ +2.00% | ❌ FAIL — Negative spread |

| 2. Price-to-NAV | Share price vs appraised asset value | ₱3.55 ÷ ₱2.41 NAV = ~1.47x | ≤ 1.10x | ❌ FAIL — Significant premium to NAV |

| 3. Occupancy & Tenants | Lease coverage; tenant quality | Long-term leases; solar operators backed by offtake contracts | ≥ 90%; creditworthy tenants | ✔ PASS — Stable, contracted income |

| 4. Debt & Rate Risk | Loan-to-Value ratio; debt structure | LTV ~25.7%; Net D/E declining toward 0.90x by 2026 | < 40–45% LTV | ✔ PASS — Gearing is manageable |

| 5. Distribution Sustainability | Payout ratio vs FFO; income trend | Payout ratio ~106% of distributable income; distributable income growing ~4% in 2026 | FFO-covered; growing trend | ✔ PASS — Sustainable with modest growth |

CREIT passes three out of five margin of safety dimensions. The business is financially sound, the income is stable, and the debt load is well within safe limits. But the two dimensions that matter most for a new investor — yield spread and price-to-NAV — both fail at the current price. That is a signal to wait, not a reason to panic.

This is the secret of successful investors that most beginners never hear:

It’s not just about knowing which stocks are good—they also know the right price to buy and when to wait. The Truly Rich Club by Bo Sanchez provides exactly that information every month. It includes specific buy-below prices for PSE stocks, including REITs. No more guessing—you already have a plan.

CREIT vs AREIT: Which Philippine REIT Makes More Sense Right Now?

If you are comparing Philippine REITs before deciding where to put your money, the natural comparison is CREIT against AREIT — the country’s largest and most diversified commercial REIT. We recently published a detailed AREIT stock analysis for 2026 where we ran the same valuation framework. Here is how the two stocks compare head-to-head.

| Factor | CREIT (Renewable Energy) | AREIT (Commercial Property) |

| Stock Price | ₱3.55 | ₱39.75 |

| Forward Dividend Yield | 5.92% | ~6.41% |

| PH 10-Y T-Bond Yield | ~6.67% | ~6.79% (at analysis date) |

| Yield Spread | −0.75% ❌ | −0.38% ❌ |

| P/NAV | ~1.47x ❌ | ~1.05x ✔ |

| Blended Fair Value | ₱2.53 | ₱37.75 |

| Buy Below Price | ₱1.90–₱2.02 | ₱29.00–₱33.00 |

| Asset Type | Solar land + plants | Office, malls, hotels, industrial |

| Portfolio Diversification | Concentrated in renewables | Highly diversified |

| Sponsor Quality | Citicore Renewable Energy Corp. | Ayala Land (largest PH developer) |

| Growth Pipeline | 1GW solar infusion planned (no timeline) | Mall infusion approved, Q2 2026 target |

| Debt Level (LTV) | ~25.7% (manageable) | ~1.2% (near zero) |

| Income Stability | High — guaranteed base rentals | High — diversified commercial tenants |

| Overall Verdict at Current Price | WAIT — Price is well above fair value. Both yield spread and P/NAV fail. | WAIT for income investors. CAUTIOUS BUY for long-term growth investors. |

The key takeaway from this comparison: both CREIT and AREIT are trading above their independently calculated fair values at current prices, and neither delivers an adequate yield spread over the risk-free rate today. However, AREIT compares more favorably on P/NAV (1.05x vs 1.47x), has a far more diversified portfolio, carries virtually no debt, and has a growth catalyst — the 2026 mall infusion — that is already approved and execution-ready. CREIT’s 1GW growth story is compelling but still at the planning stage. For a more detailed breakdown of AREIT, read our full AREIT stock analysis 2026 here.

Risks to Consider Before You Invest in CREIT Stock

No stock analysis is complete without an honest look at what could go wrong. Here are the key risks for CREIT in 2026.

1. Rising Interest Rate Environment

Philippine 10-year government bond yields have climbed sharply, driven by inflationary pressures linked to rising oil prices amid ongoing geopolitical tensions. When bond yields rise, REITs typically become less attractive to income-seeking investors — their share prices can fall even if the underlying business is fine. At the current yield spread of −0.75%, CREIT is already in negative territory. A further rise in bond yields would deepen that gap and put more pressure on the share price.

2. No Confirmed Timeline on the 1GW Solar Infusion

The planned asset infusion from CREC is the central growth catalyst for CREIT. But without a confirmed timeline, deal size, or terms, investors are essentially buying on faith that the infusion will happen and that it will be priced fairly. If macroeconomic conditions deteriorate or management decides to delay, the dividend growth story stalls — and the current P/NAV premium becomes very hard to justify.

3. Potential Share Dilution from Property-for-Share Swap

Management has signaled that the 1GW infusion may be funded through a property-for-share swap rather than debt. That means new CREIT shares would be issued to the parent company — increasing the number of shares outstanding and potentially diluting your per-share dividend if the infusion is not structured to be immediately accretive. Monitoring how this deal is structured when terms are finalized will be critical.

4. Concentrated Portfolio in a Single Sector

Unlike AREIT, which diversifies across offices, malls, hotels, and industrial land, CREIT’s entire income base comes from solar-related leases. While the renewable energy sector enjoys strong structural tailwinds, a policy change, grid disruption, or regulatory shift affecting solar energy could disproportionately impact CREIT with no other asset class to buffer the impact.

5. Variable Rent Is a Minor Risk — But Worth Noting

Approximately 3% of CREIT’s rental income comes from variable rent tied to energy generation volumes. Following the suspension of the Wholesale Electricity Spot Market (WESM) operations under a national energy emergency declaration, this small component could be slightly impacted. It is not a material risk, but it is a reminder that CREIT’s income is not 100% insulated from energy market conditions.

Final Thoughts on CREIT Stock Philippines

CREIT is a genuinely interesting REIT. It occupies a unique niche — the only renewable energy REIT listed on the Philippine Stock Exchange — and its business model is built on a foundation of long-term, contracted income that is largely insulated from market cycles. The sponsor is credible, the debt level is manageable, and the potential 1GW solar infusion could be transformational if it materializes on favourable terms.

But the current price of ₱3.55 tells a different story. Our independent valuation places the blended fair value at approximately ₱2.53 per share. At ₱3.55, you are paying a significant premium over what the fundamentals currently support. Both the yield spread and the P/NAV fail our margin of safety thresholds. The dividend you receive today is less than what a government bond pays — without any of the company-specific risk.

For value investors, the message is clear: wait. The price needs to come down meaningfully before CREIT stock in the Philippines offers adequate compensation for the risk you are taking. A level closer to the ₱1.90–₱2.02 range would satisfy our buy-below criteria. That requires significant patience — but that patience is exactly what separates investors who build wealth from those who buy at the wrong time.

For growth investors and those building a diversified REIT portfolio, the calculus is different — and the answer is more nuanced. If you are investing through cost averaging — buying a fixed amount of CREIT shares on a regular schedule regardless of price — then today’s exact entry price matters less than your long-term commitment. Cost averaging works because you naturally accumulate more shares when the price falls and fewer when it rises, smoothing out your average cost over time. You do not need to time the market perfectly. You just need to keep showing up consistently.

CREIT also makes particular sense if you are building a diversified REIT portfolio across all PSE-listed REITs. For that kind of investor, CREIT is not just another income stock — it is a unique exposure to the renewable energy sector that no other Philippine REIT offers. Holding it alongside commercial REITs gives your portfolio a layer of sector diversification. Even if CREIT’s yield spread is thinner than ideal right now, it earns its place in a multi-REIT strategy as the only clean-energy income asset on the Philippine Stock Exchange.

In Philippine REIT investing, knowing the right CREIT stock price to enter is just as important as knowing the company. Know what kind of investor you are — value, growth-oriented, or a disciplined cost averager — and invest accordingly.

You’re ready to invest. But do you have a plan?

The Truly Rich Club by Bo Sanchez answers the three most important questions every investor faces: Which stocks should you buy? What’s the right price? When is the right time? Every month, members receive a curated list of PSE stocks—including REITs—with specific buy-below prices and plain-language explanations. No complicated charts. No finance degree required. Thousands of Filipinos are already building real wealth through this system. Are you ready to join them?

DISCLAIMER

This article is for informational and educational purposes only. It does not constitute financial advice and should not be relied upon as the basis for any investment decision. All valuations are independent estimates based on publicly available information and the author’s analytical framework. Investing in the stock market involves risk, including the possible loss of principal. Always do your own research and consult a qualified financial adviser before making investment decisions.