Your Money Is Sitting Idle. These Digital Banks Will Fix That.

The best high-interest digital banks in the Philippines in 2026 are not a secret. They are just a decision most Filipinos have not made yet.

Think about where your cash is right now. Is it earning anything meaningful? Most people would say no — and they would be right.

The average Filipino keeps the bulk of their liquid savings in a low-yield account — earning almost nothing while prices around them quietly rise. Groceries cost more. Utilities climb. The peso buys a little less every year.

Meanwhile, a new generation of BSP-regulated digital banks has completely changed what is possible for everyday savers. We are talking about interest rates of 4% to 6% — and in some cases, even higher — on accounts you can open in under 10 minutes from your phone.

No long queues. No maintaining balance requirements. No complicated paperwork.

In this guide, I will rank and review the 7 best high-interest digital banks in the Philippines for 2026 — breaking down their actual rates, real conditions, hidden risks, and which one is right for your specific situation.

Why Most Filipinos Are Earning Almost Nothing on Their Idle Cash

Here is an uncomfortable question: when was the last time you actually checked how much interest your money is earning?

For most people, the answer involves opening an app, seeing a tiny number, and closing it again without doing anything about it. The problem is not awareness — it is inertia.

Digital banks in the Philippines have been offering dramatically higher interest rates for years now. But the gap between what is available and what most people are actually earning remains enormous. And that gap has a real cost.

On ₱300,000 in savings:

- At 0.5% annual interest → ₱1,500 per year earned

- At 4.5% with a high-interest digital bank → ₱13,500 per year earned

- That is ₱12,000 in missed earnings — every single year — from the same balance

Multiply that over five years and you are looking at ₱60,000+ left on the table. Not because of bad investments. Just because of where you parked your cash.

The best high-interest digital banks in the Philippines make it easy to fix this. The first step is knowing which one to choose.

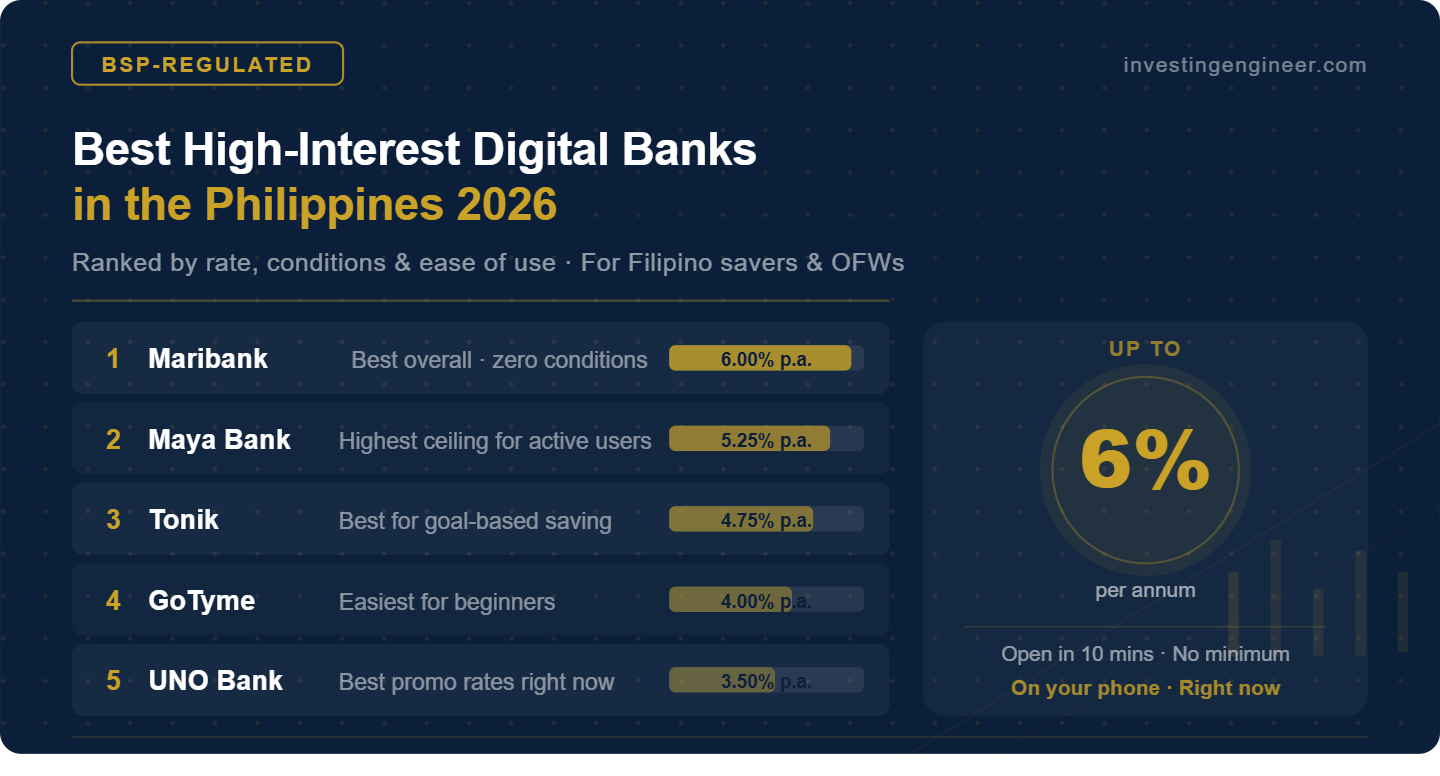

Quick Comparison: Best High-Interest Digital Banks Philippines 2026

Here is a side-by-side overview of the top digital banks currently offering the highest interest rates in the Philippines:

| Digital Bank | Interest Rate (p.a.) | Key Condition | Best For |

|---|---|---|---|

| Maya Bank | 3.5% base → up to 15% (mission-based, capped ₱100K) | Monthly spending missions required | Aggressive optimizers |

| MariBank | 3.25% (up to ₱1M) / 3.75% (above ₱1M) | Minimal conditions, tiered by balance | Passive savers |

| Tonik | 4% savings / up to 6% (Time Deposit) | Lock-in for Time Deposits | Goal-based savers |

| GoTyme Bank | 3.0% flat (no conditions, no caps) | Simple usage, no balance caps | First-time users |

| UNO Bank | 3%–3.5% savings / up to 5.75% TD | Time Deposit required for top rates | Yield hunters |

| UnionDigital | ~3%–4% | Straightforward deposit | Conservative users |

| CIMB Philippines | 2.5% base / up to ~7% (ADB growth) | Min. ₱10K ADB growth for max rate | Flexible users |

Note: All rates are approximate and subject to change. Verify current rates on each bank’s official app before depositing. All banks listed are BSP-regulated and PDIC-insured up to ₱500,000 per depositor.

Detailed Reviews: The 7 Best High-Interest Digital Banks in the Philippines

1. Maya Bank — Best for Aggressive Yield Optimizers

Interest Rate: 3.5% base / Up to 15% p.a. (mission-based, capped at ₱100K)

Maya Bank is the most talked-about name in Philippine digital banking — and for good reason. Its headline rate is the highest in the market. But here is the honest story behind that number.

Reaching anywhere near 15% requires actively completing Maya’s “missions” — spending a set amount per month, paying bills through the app, or maintaining specific balance tiers. Critically, the boosted rate applies only to balances up to ₱100,000. Everything above that cap earns the base rate of 3.5%.

Note: Maya planned to cut its base rate from 3.5% to 3.0% effective April 1, 2026, but reportedly postponed the cut. As of early April 2026, the 3.5% base rate appears to remain in effect — but monitor this closely as it may change without extended notice.

That said, even at the base rate of 3.5%, Maya is competitive. And for users who are already spending through the app anyway, the boosted mission-based rates are genuinely achievable on that first ₱100K tranche.

Pros: Highest potential yield in the PH digital banking space (up to 15%), integrated ecosystem (wallet, payments, investments, crypto), PDIC-insured up to ₱1M

Cons: Requires active effort to reach maximum rates, boosted rate capped at ₱100K balance, base rate subject to cuts with minimal notice

Best for: Power users already embedded in the Maya ecosystem who want to squeeze maximum yield from their first ₱100K.

2. Maribank (formerly SeaBank) — Best for Passive, Set-and-Forget Savers

Interest Rate: 3.25% p.a. (balances up to ₱1M) / 3.75% p.a. (balances above ₱1M)

If there is one digital bank that earns the title of the most straightforward high-interest option in the Philippines, MariBank is right at the top. The pitch is simple: deposit your money, earn daily interest, check back later. No missions. No spending targets. No promo mechanics to chase.

MariBank recently revised its savings rates — effective January 15, 2026, the rate moved to 3.25% p.a. for balances up to ₱1M and 3.75% p.a. for balances above ₱1M. While this is lower than its previous offering, it remains one of the most competitive no-condition rates available among Philippine digital banks.

A notable advantage: MariBank deposits are PDIC-insured up to ₱1,000,000 per depositor — double the ₱500,000 standard carried by many other digital banks on this list.

Pros: Competitive base rate with minimal conditions, tiered rate rewards larger balances, PDIC-insured up to ₱1M, daily interest crediting

Cons: Rate was cut in January 2026 and can be adjusted again, fewer boost opportunities vs Maya

Best for: Anyone who wants a solid, competitive rate on complete autopilot — the ideal core digital bank for passive savers.

3. Tonik Digital Bank — Best for Goal-Driven Savers

Interest Rate: ~4% (savings) / Up to ~6% (Time Deposits)

Tonik approaches digital banking with a disciplined, goal-first philosophy. Their standout feature is the “Stash” system — named savings buckets you can create inside a single account, each with its own label and target (emergency fund, travel, new phone, wedding, etc.).

For users who want to lock in higher returns, Tonik’s Time Deposit feature pushes yields up to ~6%. The trade-off is liquidity — your money is committed for a fixed period. But for savings you will not need immediately, this is one of the best guaranteed rates you will find on a BSP-regulated digital bank in the Philippines.

Pros: Excellent goal-based savings structure, higher yields for committed funds, great for building disciplined saving habits

Cons: Time Deposit lock-ins reduce access to your funds, app experience can occasionally be inconsistent

Best for: Goal-oriented savers building toward something specific — an emergency fund, a vacation, a major purchase.

4. GoTyme Bank — Best for First-Time Digital Bank Users

Interest Rate: 3.0% p.a. flat (no conditions, no balance caps)

GoTyme Bank’s biggest selling point is not its rate — it is the experience. Onboarding is genuinely smooth, the app is clean and intuitive, and the entire process from download to depositing your first peso is designed for people who have never used a digital bank before.

Backed by the Gokongwei Group (Robinsons, Cebu Pacific, and other flagship Filipino brands), GoTyme carries institutional credibility that helps ease the natural hesitation first-time digital bank users feel.

A note on the rate: GoTyme’s Go Save account was paying 3.5% p.a. previously, but was cut to a flat 3.0% p.a. effective January 2026. The good news is there are no balance caps and no conditions — what you see is what you earn, across your entire balance.

At 3%, it is not the highest yield on this list. But for a beginner making the switch to a high-interest digital bank for the first time, GoTyme removes all the friction and delivers a clean, reliable rate.

Pros: Best-in-class onboarding experience, flat rate with no caps or conditions, backed by a trusted Philippine conglomerate

Cons: Rate was cut from 3.5% to 3.0% in January 2026, no advanced yield upside compared to Maya or Tonik

Best for: Anyone opening their first high-interest digital bank account who wants a simple, predictable, no-surprises experience.

5. UNO Digital Bank — Best for Yield Hunters

Interest Rate: 3.0%–3.5% savings (UNOReady) / Up to 5.75% via Time Deposits (UNOearn / UNOboost)

UNO Digital Bank is one of the more aggressive competitors in the Philippine digital banking space. If you are willing to commit funds to a Time Deposit, UNO’s TD products (UNOearn and UNOboost) push yields up to 5.75% p.a. — among the better TD rates available right now.

On the savings side, UNO’s UNOReady account pays 3.0%–3.5% p.a. — competitive for a fully liquid account, though lower than some earlier estimates. The real yield advantage kicks in when you move funds into their TD products.

As a newer entrant still building its user base, UNO tends to run attractive promos. The trade-off is a shorter operating track record compared to more established names like Maya or MariBank.

Pros: Strong TD rates (up to 5.75%), competitive liquid savings rate, aggressive promos as an emerging player

Cons: Shorter operating history, best rates require locking funds in a TD, rate volatility as promos cycle

Best for: Savers who want above-average TD yields and are comfortable locking funds for a fixed term.

6. UnionDigital Bank — Best for Stability-First Users

Interest Rate: ~3%–4%

UnionDigital Bank is the digital banking arm of UnionBank of the Philippines — one of the country’s most established commercial banking institutions. For users who want the benefits of a high-interest digital bank but with the backing of a full-scale regulated commercial bank, UnionDigital is the natural fit.

Its rates sit at the lower end of this list, but the institutional trust, infrastructure reliability, and seamless integration with the broader UnionBank ecosystem make it a strong choice for conservative users.

Pros: Backed by UnionBank’s established commercial banking infrastructure, consistent and reliable performance

Cons: Lower yield ceiling compared to SeaBank, Maya, and Tonik

Best for: Conservative savers who prioritize institutional stability and reliability over chasing the highest available rate.

7. CIMB Bank Philippines — Best for Flexible Savers

Interest Rate: ~2.5% base / Up to ~5% with promos

CIMB Bank is one of the most recognized digital banking brands across Southeast Asia, with a well-established presence in the Philippines. Their base rate is lower than most competitors on this list, but promotional mechanics can push yields meaningfully higher for qualifying users.

CIMB’s regional scale and brand familiarity give it a credibility edge, particularly for users who may have encountered the brand in other ASEAN markets.

Pros: Strong regional brand, BSP-regulated, flexible product structure

Cons: Lower base rate, promotional conditions can be complex to navigate

Best for: Users who value brand recognition and regional credibility while still earning above-average digital bank rates.

How to Choose the Right High-Interest Digital Bank for You

Not every high-interest digital bank in the Philippines is the right fit for every person. Here is how to think through your decision:

1. Decide: Active Optimizer or Passive Saver?

Maya Bank and UNO offer the highest ceilings — but they require effort to reach. If you want to spend time optimizing missions, tracking promos, and rotating funds, these give the best upside.

If you want to deposit and forget, SeaBank or GoTyme are your best fits. High rates. Minimal conditions. Done.

2. Liquidity vs. Higher Returns

Tonik’s Time Deposits offer some of the best guaranteed rates available — but they require a lock-in period. Before committing funds to a Time Deposit, make sure you will not need that money during the lock-in window.

A good rule: keep at least one to two months of living expenses in a fully liquid, no-condition account. Lock only what you are confident you will not need.

3. Do Not Chase Headlines — Calculate Your Real Yield

When a digital bank advertises “up to 10%” — always ask: up to 10% on how much? Under what conditions? With what cap?

Many promo rates apply only to the first ₱50,000 to ₱100,000. The blended yield — what you actually earn across your full balance — is almost always lower than the headline number. Calculate realistic expected earnings, not the best-case scenario.

4. Confirm PDIC Insurance

Every bank on this list is BSP-regulated and PDIC-insured — but coverage levels vary. Most digital banks carry the standard ₱500,000 per depositor coverage. However, Maya Bank and MariBank are both insured up to ₱1,000,000 per depositor — double the standard amount.

Always verify the specific PDIC coverage level of each bank you use. If your deposits in a single institution approach or exceed the coverage cap, split the remainder into a separately insured digital bank.

The Smart Allocation Strategy: How to Use Multiple Digital Banks in 2026

The smartest Filipino savers in 2026 are not picking just one high-interest digital bank. They are building a system across multiple accounts — each one serving a specific purpose.

Recommended Digital Bank Allocation Framework

40% → Stable high base rate (MariBank / GoTyme) — your core liquid digital savings

30% → High-yield optimizer (Maya / UNO) — actively managed for maximum return

20% → Time deposits (Tonik) — locked savings earning the highest guaranteed rate

10% → Emergency access account (UnionDigital / CIMB) — reliable fallback with solid backing

The core principle: each account has a job. Your emergency fund lives in a fully liquid account. Your medium-term savings earn the highest available rate. Your locked funds earn even more via Time Deposits.

Key Principles for Your Digital Bank Strategy

- Split across at least 2–3 digital banks for both yield optimization and risk reduction

- Monitor promos quarterly — rotate funds when a materially better offer appears

- Do not over-optimize: chasing a 0.3% rate difference on ₱50,000 yields ₱150 extra per year. Not worth the complexity.

- Review your allocation every 3–6 months and adjust as the market shifts

5 Hidden Risks of High-Interest Digital Banks Most Filipinos Miss

The best high-interest digital banks in the Philippines are genuinely excellent products. But here is what most comparison articles do not tell you:

1. Promo Rate Traps

That headline “up to 10%” often applies only to the first ₱50,000–₱100,000 of your balance. Everything above that cap typically earns a much lower rate. Always model what your entire balance actually earns — not just the promotional tranche.

2. Balance Interest Caps

Some digital banks cap the total balance eligible for their high-interest rate. Funds deposited above the cap may earn a fraction of the advertised rate. Check the fine print before moving large sums.

3. App Downtime Risk

Every digital bank is an app-first product. When scheduled maintenance or unexpected outages occur — and they do — you may be temporarily unable to access or transfer your funds. Always ensure you have liquidity accessible through at least one alternate channel.

4. Rate Changes With Little Notice

Digital banks are not bound to long-term rate commitments. They can and do adjust interest rates — sometimes with minimal advance notice. The best high-interest digital bank today may lower its rates next quarter. Review your accounts every three months.

5. Concentration Risk

Keeping all your liquid savings in a single digital bank — even an excellent one — exposes you to unnecessary concentration risk. Splitting across two or three PDIC-insured accounts eliminates this problem at zero cost.

Beyond Digital Banks: The Next Step for Building Real Wealth

Here is the truth that every honest financial article should tell you:

Even the best high-interest digital banks in the Philippines — at 4% to 6% per year — cannot build meaningful long-term wealth on their own.

With Philippine inflation running at 3%–4% annually, a 5% digital bank return gives you a real return of roughly 1%–2% after inflation. That keeps your purchasing power intact. It does not grow your wealth significantly.

If your goal is financial independence, a retirement fund, or leaving something behind for your family — digital banks are the foundation. They are not the destination.

The next step is investing. And for most Filipino beginners, the Philippine Stock Market is the most powerful, accessible, long-term wealth-building vehicle available.

But here is where most people get stuck: they do not know how to start. The stock market feels complicated. They are afraid of losing money. They do not know which stocks to buy.

💡 This Is Exactly What the Truly Rich Club Was Built For

The Truly Rich Club (TRC), founded by Bo Sanchez, is a membership community designed specifically for Filipinos who want to invest in the Philippine Stock Market — but want clear, guided, beginner-friendly direction rather than figuring it out alone.

As a TRC member, you get:

- A model stock portfolio — specific stocks recommended, so you always know what to buy

- Monthly newsletters in plain Filipino-friendly language explaining market movements

- A community of thousands of like-minded Filipino investors learning and growing together

- Bo Sanchez’s proven long-term, values-based investing philosophy

TRC is not a get-rich-quick scheme. It is a guided, systematic approach to building wealth through disciplined long-term stock investing — the same approach that has worked for tens of thousands of Filipino members.

Final Verdict: Which Is the Best High-Interest Digital Bank in the Philippines 2026?

Here is the complete summary of the best high-interest digital banks in the Philippines for 2026:

| Category | Winner | Why |

|---|---|---|

| 🏆 Best Overall | MariBank | Consistent base rate (3.25%–3.75%) with zero conditions — the cleanest no-effort high-interest digital bank for most Filipinos. |

| 👶 Best for First-Timers | GoTyme Bank | Beginner-friendly interface and onboarding, backed by a trusted retail group. Flat 3% rate with no conditions or caps. |

| 🚀 Best for Max Yield | Maya Bank | Highest potential ceiling (up to 15%) for active users willing to complete monthly spending missions on capped balances. |

| 🎯 Best for Goal-Based Saving | Tonik Bank | Structured lock-in Time Deposits (up to 6%) are perfect for saving toward specific financial targets. |

| 🛡️ Best for Stability | UnionDigital Bank | Reliable rates backed by UnionBank’s established digital infrastructure. |

The right answer depends on your goals, your habits, and how actively you want to manage your digital banking. What is certain is this: any of the seven digital banks on this list will put your money to work far more effectively than leaving it idle.

Pick one that fits your style. Open the account. Start earning. Then build from there.

Conclusion: Your Money Deserves a High-Interest Digital Bank in 2026

The best high-interest digital banks in the Philippines in 2026 have made it easier than ever to earn a meaningful return on your liquid savings.

4% to 6% interest. BSP-regulated. PDIC-insured. App-based. Accounts opened in minutes. No long queues. No minimum balance drama.

There is no longer any good reason to let your money sit idle. The only question is which high-interest digital bank you will start with — and when.

Once your digital banking system is set up and running smoothly, your next move is to start building actual long-term wealth through investing. And that is exactly what the Truly Rich Club is designed to help you do.

Related reading: Truly Rich Club Review 2026: Is Bo Sanchez’s Membership Still Worth It?

New to investing? Start here: The Complete Beginner’s Guide to Investing in the Philippines

Frequently Asked Questions: Best High-Interest Digital Banks Philippines 2026

| Question | Answer |

|---|---|

| Which digital bank has the highest interest rate in the Philippines 2026? | Maya Bank has the highest ceiling — up to 15% p.a. — but this applies only to capped balances (₱100K) and requires completing monthly spending missions. MariBank offers the most consistent high base rate (3.25%–3.75%) with almost no conditions, making it the most reliable no-effort option for most Filipinos. |

| Are high-interest digital banks in the Philippines safe? | Yes — all the digital banks featured in this article are BSP-regulated and PDIC-insured. Coverage varies: most banks carry ₱500,000 per depositor, while some (including Maya Bank and MariBank) carry ₱1,000,000 in PDIC coverage. Always confirm the coverage level with your specific bank before depositing large sums. |

| Can I open multiple digital bank accounts at the same time? | Absolutely. There is no rule against holding accounts across multiple digital banks. Many savvy savers split their money across 2–3 apps to maximize interest, maintain liquidity, and reduce single-bank risk. |

| What is the difference between a base rate and a promo rate? | The base rate is what the bank always pays, regardless of your behavior. The promo rate is conditional — it requires spending targets, missions, or specific balance tiers to unlock. Always calculate what you actually earn on your full balance, not just the headline number. |

| What does PDIC insurance cover for digital banks? | PDIC insures your deposits if a bank closes. Coverage levels vary: most BSP-licensed digital banks carry ₱500,000 per depositor, but some — including Maya Bank and MariBank — carry ₱1,000,000 in PDIC coverage. If your deposits in one bank exceed the coverage limit, split the remainder into another insured institution. |